Strait of Hormuz and Oil and Gas

Introduction

The Strait of Hormuz is a strategic waterway located between Iran and Oman, serving as a vital connection between the Persian Gulf, the Gulf of Oman, and the Arabian Sea. A significant portion of the world’s oil exports from Gulf countries passes through this narrow passage, making it one of the most important chokepoints in global energy trade.

Throughout the years, geopolitical tensions and threats of closure in the Strait have led to sharp reactions in oil markets, reflecting its critical role in energy supply chains. This post will delve deeper into the significance of the Strait of Hormuz, exploring its economic, political, and strategic importance.

Volume of Petroleum and LNG Transported Through the Strait

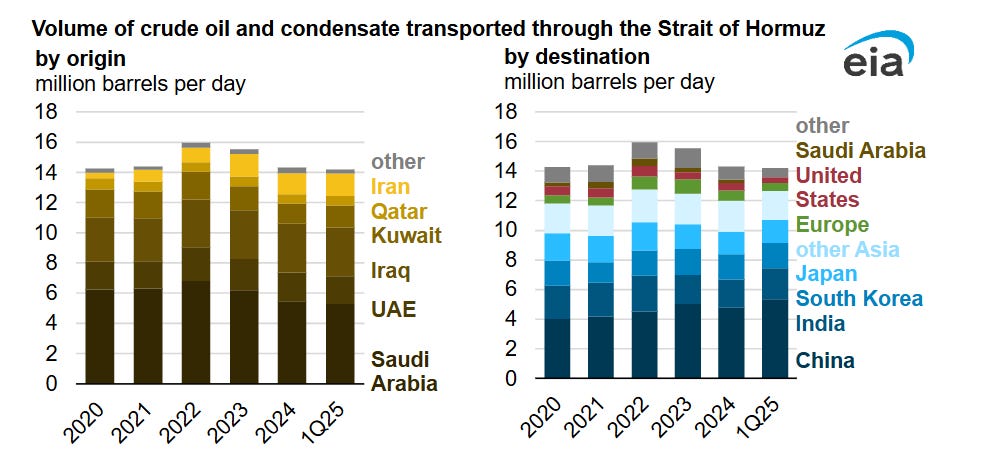

In 2024 about 20 million barrels of oil per day pass through the Strait. That is around 20% of global oil consumption. Of that, crude oil condensates flows made up around 16 million b/d, and petroleum products made up another 4.5 million b/d. Most of the crude and condensate that pass through the Strait is destined for Asia.

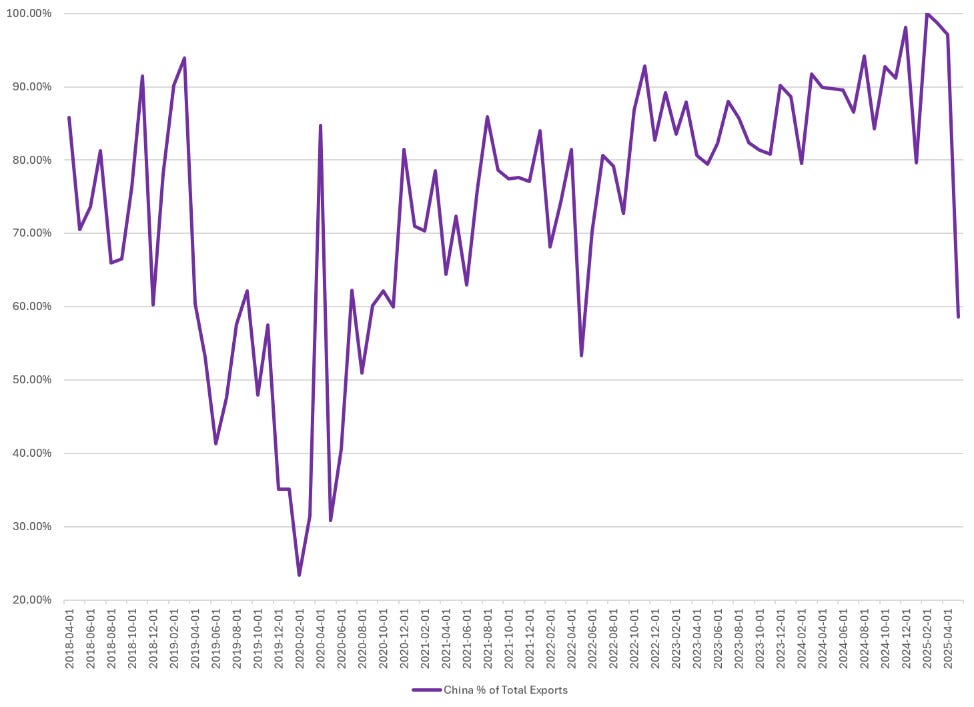

China has been a major buyer of Iranian crude. The chart below tracks oil exports and shows a breakdown of trade flows. From the graph, it’s clear that China accounts for the vast majority of Iran’s crude exports. Historically, Iran has exported approximately 1.5 million barrels per day to China.

Looking past the petroleum transported through the Strait we start to look LNG, most of which is being exported from Qatar. Hormuz carried about one-fifth of global LNG.

Recently, there has been considerable concern about the potential closure of the Strait of Hormuz. However, much of that worry has dissipated as the geopolitical risk premium has continued to fade. Looking at overall trade volume and transit calls, activity is currently in line with historical norms.

The graph below shows trade volume and transit calls through the Strait of Hormuz, highlighting how oil markets have historically reacted during periods of heightened geopolitical risk.

Alternative Routes

There are workarounds currently in place. The East-West Crude Oil Pipeline (Abqaiq-Yanbu NGL Pipeline) in Saudi Arabia can handle around 7 million barrels per day and has been operating below capacity. The UAE also has a pipeline to the port of Fujairah, with a maximum capacity of 1.8 million barrels per day. However, this pipeline has been used more frequently for regular flows recently, leaving less spare capacity available.

Iran has the Goreh-Jask export terminal on the Gulf of Oman, but the pipeline’s effective capacity remains around 300,000 barrels per day. According to the EIA, in 2024 Iran exported less than 70,000 barrels per day through ports using the Goreh-Jask pipeline and ceased loading cargoes after September 2024.

Effects of a Hypothetical Closure

China is not the most vulnerable—despite being the world’s largest oil importer and a major customer of Iranian crude. Currently, around 50% of China’s oil imports—approximately 3.5 million barrels per day—pass through the Strait of Hormuz. Looking beyond China, about 85% of the crude oil and condensate, and 83% of the LNG that moved through the Strait, was destined for Asian markets. Excluding China, India, Japan, and South Korea were among the top destinations for crude oil transported through the Strait, collectively accounting for 70% of all Hormuz crude and condensate flows in 2024.

Effects on China?

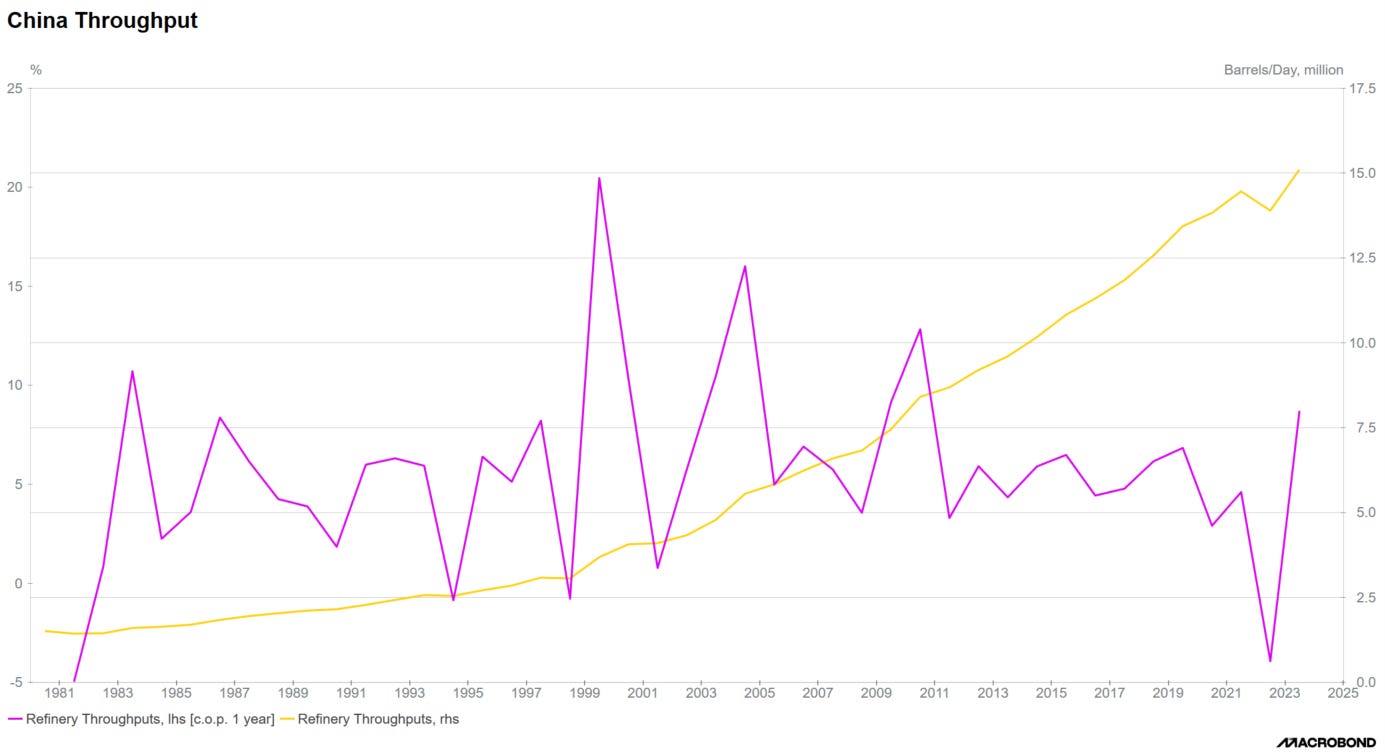

China has seen an increase in refinery throughput over the years. Currently for 2024 Chinese throughput is around 15 million b/d and rose almost 7.5% relative to the previous year.

Looking past this, Chinese onshore crude inventories are around 1.2 billion barrels. We’ve also seen some of the teapot refiners begin to slow down, and overall demand from China appears to be easing. So again, in a hypothetical future scenario, China would likely have enough reserves to weather a supply disruption. As Vortexa graph below highlights the decline in sanctioned crude point towards higher stocks, and weaker demand.

Per Vortexa, Chinese refinery runs fell 3% year-over-year, returning to near the three-year seasonal average, indicating lower utilization despite recent capacity growth. The decline is mainly due to delayed maintenance among teapot refiners and weak margins. State-run refiners also had significant capacity offline in May due to peak maintenance, but throughput may rebound in June as turnarounds conclude. Stockbuilds could moderate in June before rising again in July–August, driven by cheaper OPEC barrels following recent policy changes.

What’s Next for Oil?

Now, as it relates to the geopolitical premium in oil: absent a major supply disruption, we expect oil to move somewhat higher in the near term before fading.

The geopolitical risk premium in oil has largely dissipated, and the only sustainable path for prices to move higher would be through a meaningful disruption in supply.

Over the next 1–2 months, we expect oil to settle in the mid-$60s range.

The options market, we have seen a significant increase in the ratio of put volume to call volume. This suggests that we could begin to see further downside price risk for WTI.

The put/call ratio is back at 1, climbing from around 0.5 to approximately 1.0. As shown in the top chart below, when the put/call ratio was below 1 (shaded area), crude prices tended to rise and vice-versa.

As mentioned above, I expect oil to remain around $60 over the next few months, absent any geopolitical tensions that could cause temporary spikes. While the Strait of Hormuz is extremely important, there are alternative routes that could help mitigate some of the pressure from a potential closure. Unless there is a significant shift or a major supply constraint, I do not anticipate higher oil prices based on current conditions.