Fed Will Back Off

One of the things I’ve been vocal about is the Fed’s inability to be able to sustain interest rates, and their backing off from the current “tightening regime.” Yes, I put tightening in quotes because the Fed is not really tightening monetary policy, as monetary is already tight. The inability of the Fed to sustain rate hikes has many factors. Some of the factors are the lack of YoY increase in the volume of credit issuance, the Fisher Effect, what swap spreads are telling us, and lastly what the cross-currency basis swap market is telling us currently about the inability of banks to have access to the wholesale dollar funding market. All of these things will play a role in my thesis on why the Fed is not able to raise interest rates.

Starting with Milton Friedman who said, “After the U.S. experience during the Great Depression, and after inflation and rising interest rates in the 1970s and disinflation and falling interest rates in the 1980s, I thought the fallacy of identifying tight money with high-interest rates and easy money with low-interest rates was dead. Apparently, old fallacies never die.” This is one of the most crucial ideas to being able to understand the Federal Reserves' (Feds) ability to raise interest rates for a sustained amount of time. As the chart below indicates, the pretext for every rise in interest rates was YoY volume of credit issuance. This chart was beautifully done by Maroon Macro, who writes the Monetary Mechanics substack. As he states in his article when most people think of low rates they assume that credit must be abundant. However, this could not be further from the truth. As can be seen in the graph below that it is the exact opposite, and why is that? Well simple as Maroon pointed out low rates can only spur demand. Said, in other words, low rates may change consumers' propensity to borrow, or want to consume, however, that is only the demand side and we must also look at the supply side i.e. the banks and institutions that decide who to lend to. Based on this one fact and in my opinion, the only way to see sustained higher rates is through increased YoY volume of credit issuance, as has been a pretext almost every time in history.

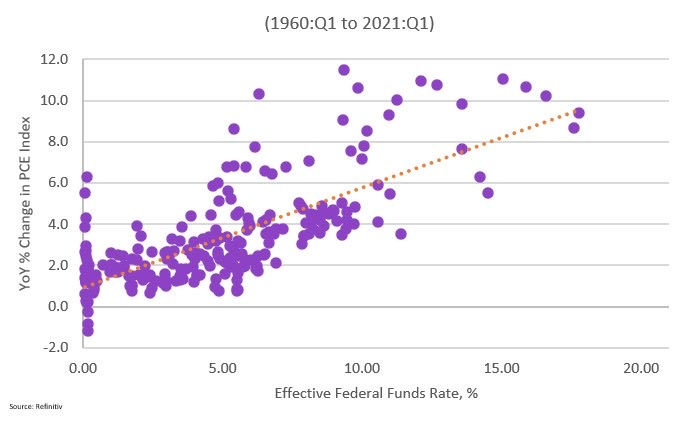

Now my next point is purely economic theory and was the idea of a great economist, Irving Fisher. The chart below denotes the idea. What we do in this model is that R = r + π. So r is the real rate of interest, π is the inflation rate, and R is the nominal rate. We can see in this model, and as is explained in the graph that R increases there is a 1-1 increase in r. However, this is just in the short run, and as time pushes us along r moves back to its long-run level. In the long run, r moves back into equilibrium, and π increases 1-1 with R. There is another graph below that shows similar adjustments, as this was also pulled from the same research paper that was written by Stephen D. Williamson and updated. As can be seen in this chart 3 the slope is consistent with the idea that inflation tends to rise, as the fed funds rate increases as well.

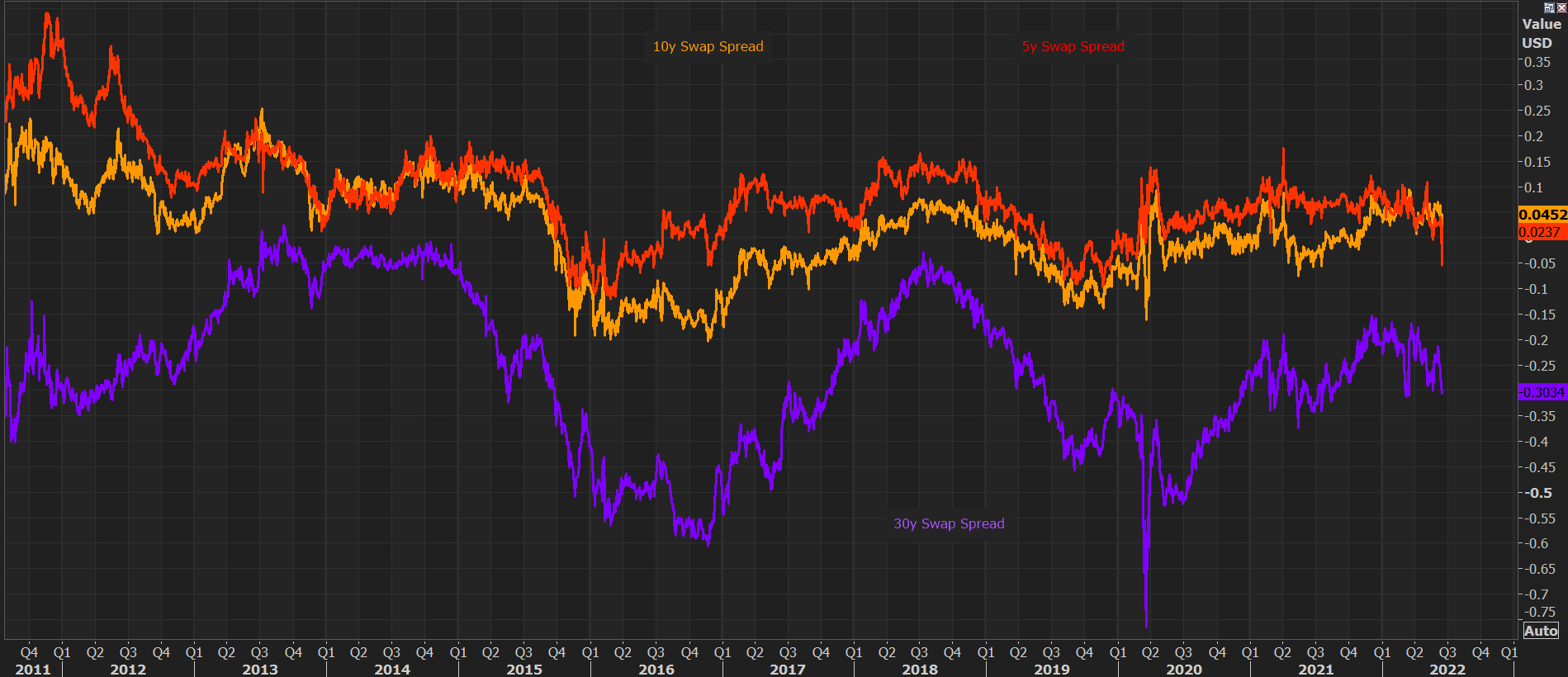

The next problem I see is shown in the chart below. I will write a more in-depth post on this at some point, but the chart below is showing the swap spreads of different tenors. A deviation in covered interest parity can be seen. This is most likely due to balance sheet (B/S) constraints, and Repo agreements could reduce B/S constraints however we are not seeing that. The probability to see a deflation period is high, as those B/S constraints are preventing participants from the arbitrage opportunity. A slight reflation was seen in 2018, however, that was short-lived. This is another further indicator of the market not selling what the fed is buying.

Finally, we will look at the cross-currency basis swap. In my opinion, this is the ultimate indicator of the Fed's inability to raise rates. To keep things simple, and without getting too technical think of cross-currency basis swaps as premiums charged for perceived dollar shortage, and for counterparty (bank) risk. When we do not provide the world with enough dollars there is a dollar shortage, and that dollar shortage puts pressure on institutions abroad. The more negative the basis, the higher the premium US counterparties are wanted for swapping USD. We have almost hit lows that haven’t since the beginning of the pandemic as measured by the G7 cross-currency basis swap index vs dxy. This is indicating US monetary policy and fiscal policy has massive implications for countries abroad. If the Fed keeps continuing this policy of tightening it is going to have real repercussions abroad. If banks abroad are unable to access the wholesale dollar funding market, you could see rising bank risk, as is being seen in Europe and this could bring about contagion risk. The contagion would be purely from a liquidity standpoint, and this is the biggest factor that would make the Fed rotate off the current tightening policy.

In conclusion, I am a firm believer that the Fed will back off. There are many different aspects that have been discussed in this article including monetary theory, swaps, and cross-currency basis swaps. All of these have big impacts on the broader idea that the Fed would be able to continue raising rates. This is something that people should look at and take into account in terms of future Fed hikes.

intersting. thanks for posting

Great Explanation!

Though I agree with you that the Fed will eventually back down, but the biggest question is when. Last time, they raised rates to 2.5% before starting another QE. This time they are "targeting" a neutral rate, which is around 2.5-3% as of now.

Will a "crisis" in European bonds or a currency crisis in Asia lead them to back off? The USD shortage and the weakness in the yen and euro have huge implications for weaker economies with low forex. The crisis this time will be elsewhere for sure, but the response of the Fed will be keenly watched (another QE or just a halt of QT and hiking rates).