De-dollarization? Don't Kid Yourself The First BRIC Hasn't Even Been Laid

De-dollarization? Don't Kid Yourself The First BRIC Hasn't Even Been Laid

This post is coming from all the hype that we have all heard around the end of the dollar. Most of this is completely unfounded, and the beginning of this “de-dollarization” hasn’t started, nor will it ever start. Now some might say that this is a bold claim, but some things need to be understood in how this all functions, and what I see today that has brought me to the conclusion that the dollar will reign supreme for much much longer. In this I will touch on the importance of invoicing, settlement, FX Swaps, and other issues around this and why I believe the idea of BRICS is so overblown.

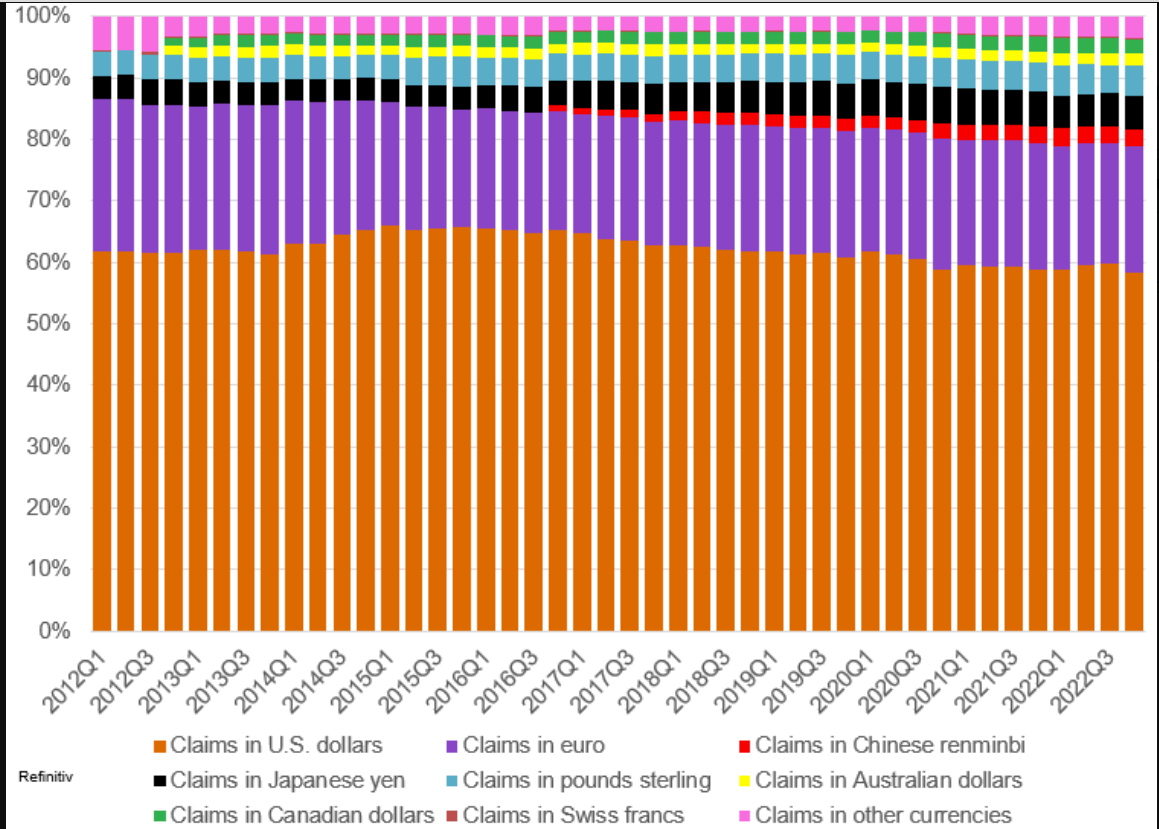

If we were expecting dollar demand to decrease, one would expect to see a draining of Central Bank Forex (FX) Reserves. While the dollar use in terms of reserves has declined it is not something that worries me all that much. Below in (Figure 1.) you can see the overall compensation of globally disclosed FX reserves. On a quarter-over-quarter basis, (QoQ) USD share of globally disclosed reserves is up 47bps, and accounts for about 58% of all globally disclosed FX reserves, the renminbi accounts for about 2.69%. Now one can make the argument that the growth of the renminbi in reached that mark, or said another way the rate of change in the renminbi make up global reserves has seen growth much more rapid than GBP, CHF, or JPY but we have to remember this is coming off a very low base in regards to the renminbi growth rate. Currently, the global reserves of the renminbi are around 300 billion, but in a global market where the nominal figure is roughly 12 trillion, this growth is extremely small.

Now for the most important thing to understand, the difference between dollar settlement and dollar invoicing. Commodities and other things have long been settled in currencies other than the dollar this is nothing new, nor does it matter all that much. What is more important is dollar invoicing, now many people conflate the two things, but they are dramatically different. For this, I will be pulling some things from the paper from the IMF “Patterns in Invoicing Currency in Global Trade” which discusses in depth what invoicing is, and how it affects trade as well as other factors which will be discussed below.

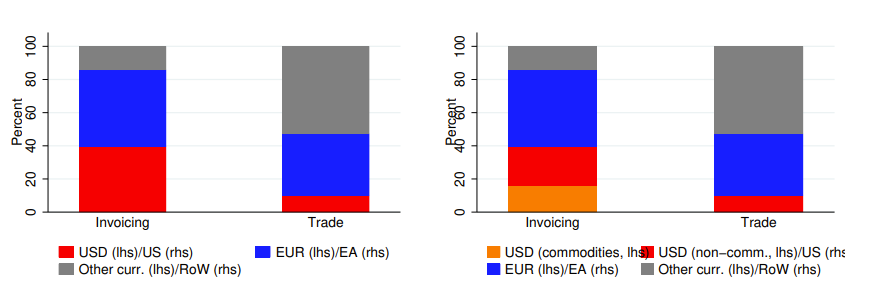

First of all, what is invoicing? The IMF put it best “…it postulates a dominant currency paradigm whereby export prices are instead set in a so-called vehicle currency (Gopinath, 2015; Gopinath et al., 2020). A key observation underlying this paradigm is that most global trade transactions are invoiced in just a few currencies – most often the US dollar, sometimes the euro – regardless of the countries involved in the transaction” (Boz, et al., 2020). This leads to some very interesting concepts in the role that the dollar plays within the trade, as well as overall global financial markets below (Figure 2.) we can see something quite interesting.

(Boz, et al., 2020)

What we see from this is that the share of exports that are invoiced in USD is larger than the share of exports that arrive at the shores of the USA, or are destined for the United States (Boz, et al., 2020). This gap between exports invoiced in dollars vs exports destined for the USA shows the role that the USD has in global exports. The phone above on the right panel of Figure 2 helps establish that the dollar's role in global trade is more than just the petrodollar or commodities and that once you deduce out exports from both invoicing and export shares the dollar share of invoicing (23%) exceed by a large gap share of exports destine for the US (10%) (Boz, et al., 2020). Now we can even break this down on the country level where we can see the difference between the dollar and euro in invoicing (if anyone would challenge the dollar it would be the euro).

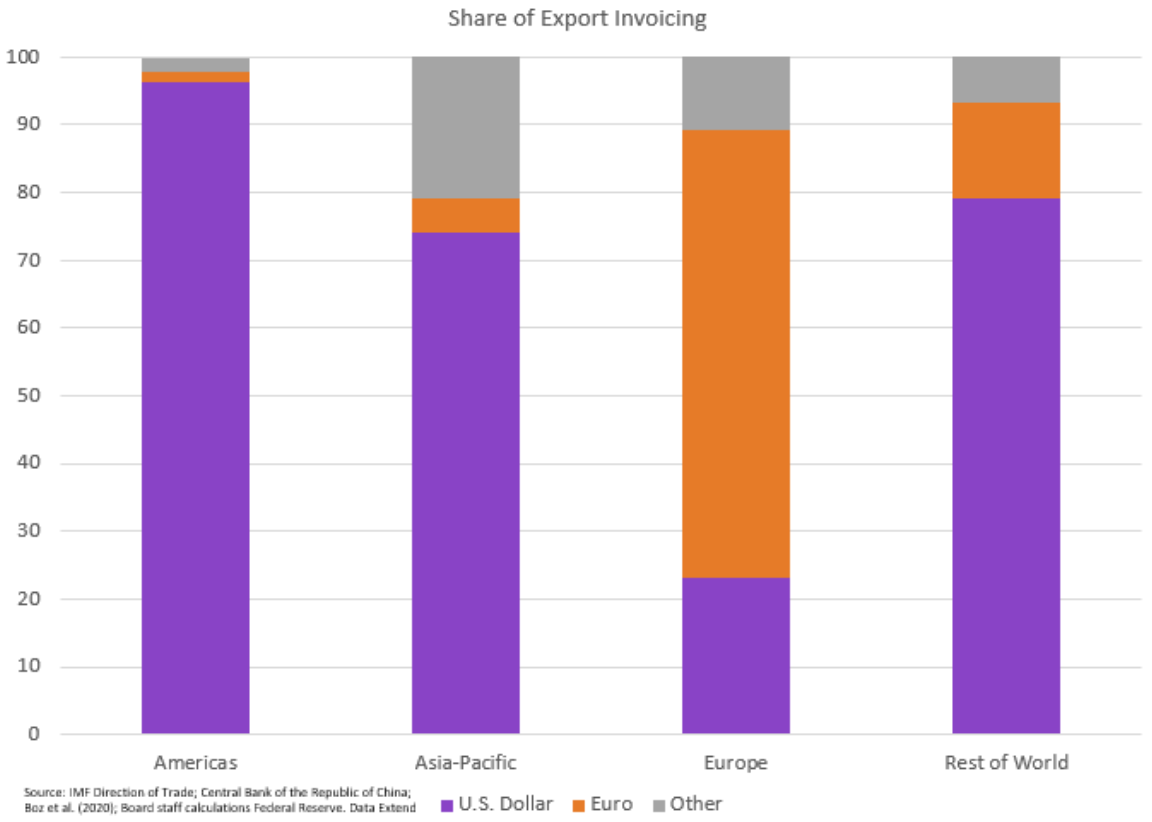

Thus one can already see the massive role that the USD plays in global trade invoicing (Boz, et al., 2020). Below (Figure 3) on the left panel it compares the shares of countries' exports to the US in total exports with the share of their exports which are invoiced in USD; in a vast majority of the cases, the latter is much greater than the former (Boz, et al., 2020). Now on the right panel of Figure 3, the euro does have a dominant role in global trade but it plays a role where it is predominant on a regional basis (Boz, et al., 2020). In particular, non-EA European countries and several countries in Africa utilize the euro who use the euro for invoicing more than just in their exports to the EA (Boz, et al., 2020). As mentioned Figure 3 helps one see the idea of the global dominance the USD has, while the EUR has more of a regional dominance (Boz, et al., 2020).

(Boz, et al., 2020)

Next, we look at the exchange rate pass-through, as the dollar invoicing plays a big role in the pass-through of exchange rate fluctuations to prices, thus a higher dollar invoicing shares massive increases in dollar pass-through (Boz, et al., 2020). The estimates indicate that a 100bps increase in dollar invoicing share leads to a 30bps-60bps increase in the dollar pass-through (Boz, et al., 2020). This will be a significant point to remember in the BRICS argument. Now we can see from above why dollar invoicing has brought stability into overall invoicing patterns (Boz, et al., 2020). This has now shown that countries who invoice more in dollars or any currency will tend to experience great dollar exchange rate pass-through to their import prices, and also their trade volumes become more sensitive to fluctuations in these exchange rates (Boz, et al., 2020). This point is significant for the BRICs debate, as we have seen import prices and trade volumes become way more sensitive to fluctuations in exchange rates, if we look at the renminbi the Chinese have had a terrible time fighting both deflation and inflation in terms of exchange those who do have to trade or invoice in renminbi granted it is relatively small. The fluctuations that have ravaged the renminbi as pointed out above then have impacts on pricing, and thus trade volumes. So if BRICs were to work the first thing they would have to do is smooth out the volatility of currencies to allow for stability within invoicing patterns.

This is the first issue with the BRICs is the inability to be able to invoice due to the stability, as well as the effects on pricing and trade volumes. If you had wild volatility or fluctuations in the value of the currency this could bring trade to a standstill. With the wide swings in exchange rates as well you get the issue of either deporting deflation/inflation depending on the movements within the currency paradigm as this affects the underlying pricing mechanism. Figure 4 below we can see the overall components of overall invoicing which shows all the different components of currency invoicing. We can see the overall breakdown, and the only place that we see a large share of invoicing in currencies other than the dollar is in the Asia Pacific, as well as Europe. However in other parts of the world, most of this is made up of dollars almost 80%, Asia Pacific 76%, North America 95%, and the lowest area is Europe where it is roughly 25%.

So what does this mean for BRICs well we can see from the above thus far the renminbi is not being utilized as a unit of account for money of the world's Central Banks it makes up a relatively small share. Next, we see the issues that a currency like the renminbi would have in terms of invoicing, therefore accounting unit for international trade would have many issues and is not being utilized as such globally. Next, we are going to look at its utilization within trading global financing assets debts, and equities.

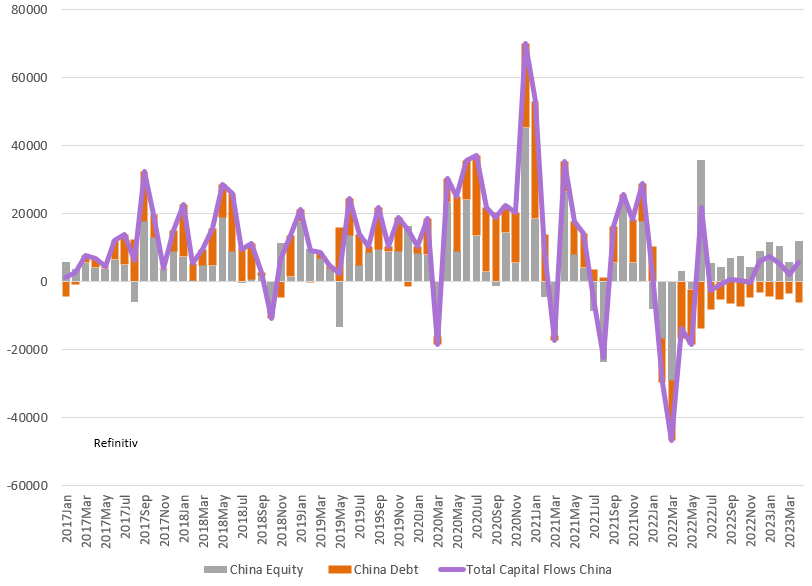

Over the past year, China has seen heavy selling of its debt, and we have seen the demand for Chinese debt completely disappear. The flows we have seen have been into equity flows which is not surprising, but never the less to really replace the dollar as a reserve currency you would want to see investor appetite to hold Chinese bonds and currently, there is none. So these large and persistent outflows we have seen over the last year are a massive hard sell for China achieving reserve currency status. The overall composite of current flows is shown below (Figure 5).

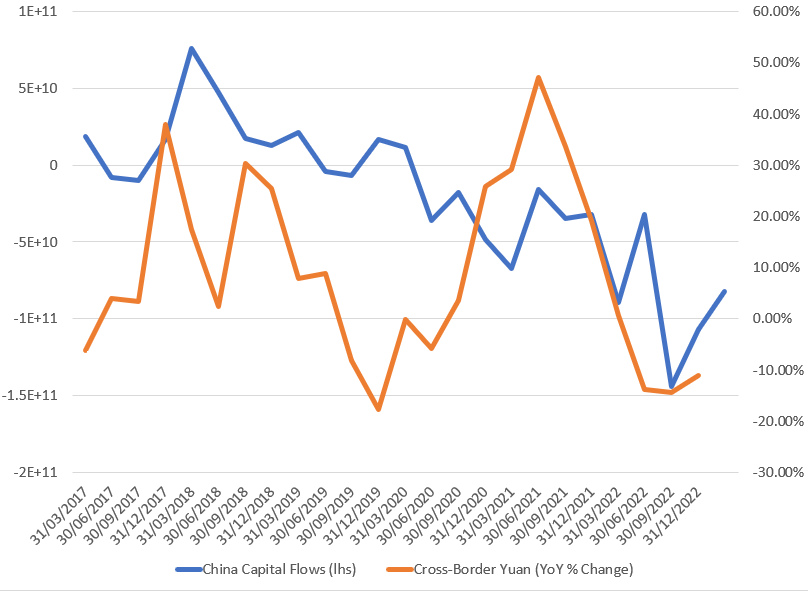

Below (Figure 6) is another chart that shows Capital outflows and FX reserves, so far China is still in negative territory so outflows continue within China, albeit they have eased in the recent quarter. What is interesting is these outflows have not flowed through into FX reserves, this is odd as this should always flow through into FX reserves or is normally the case. What we are seeing is that these outflows are from the renminbi not only putting pressure on the renminbi bought are getting converted into offshore dollars. So this can be brought down to changes in cross-border flows into the dollar, which are not accounted for in measuring currency outflows. Everyone was talking about the PBOC swap lines blowing out, and I think this was also a function of people converting yuan to dollars. Figure 7 shows the current decrease in flows from the cross-border yuan. This will be discussed more next as well.

I will start by looking at turnover volumes, from reporting dealer banks. Looking at Figure 8, it is clear that the dollar is the most utilized currency by a substantial margin, and the continued growth has been driven by inter-dealer and dealer-financial institution FX swaps. One can see how low the BRIC nations are ranked at the bottom, and while the growth again has been impressive it was coming off a very very low base. During the same period, we are seeing more rapid growth in USD compared to BRICs where the growth rate has been pretty muted since 2016.

Now we are looking at the funding gap for dollars and how this is within the BRICs nations. What we see is that the funding gap is pretty evenly distributed across the BRIC nations, which means that the gross dollar-denominated positions of the banking system within BRIC nations are long-dollar. Put another way this is the banking system saying that they want to borrow dollars, and the dollars are lent by the US banks. So the financial system within the nations that are supposed to be replaced with the dollar is saying from a financial market standpoint they want more dollars than they currently have. This picture is painted in Figure 9.

In closing, we can see that many things are pointing to the fact that the dollar is not going anywhere anytime soon. We have seen the inability of China to be a currency that wants to be held as a unit of reserves for Central Banks, it is not being utilized for accounting of international trade broadly speaking, and as a transaction currency for global financial assets, we are not seeing that either. The large outflows from investors and the unwillingness to hold Chinese debt seem to be another factor painting the picture that the trust is not there. From where it stands today it seems that the dollar will continue to be the currency vehicle of choice not just for global trade, but for global financial markets for a long time to come.

Excellent piece. Glad to see you back writing on Substack!

Thank you for this amazing succinct, and well structured analysis!